In case you haven’t noticed, the bulls are running wild on Wall Street. Following the 2022 bear market, all three major stock indexes — the ageless Dow Jones Industrial Average, broad-based S&P 500, and widely tracked Nasdaq Composite — have recently reached record-closing highs.

While a number of factors have contributed to this outperformance, including stronger-than-anticipated U.S. economic growth, the lion’s share of the heavy lifting has been done by the “Magnificent Seven.”

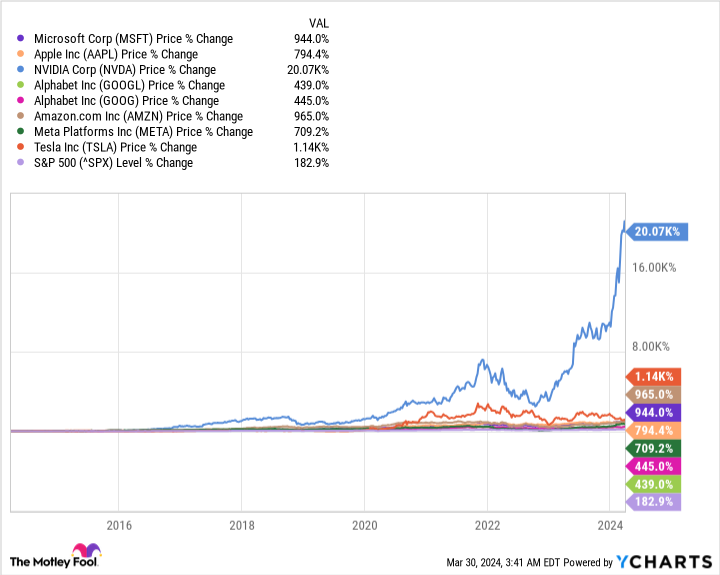

The Magnificent Seven stocks have taken Wall Street to new heights

The Magnificent Seven are, as the name implies, seven of the largest and most-influential public companies. Listed in order of descending market cap, the Magnificent Seven stocks are:

There are two reasons investors have flocked to these seven businesses for years. The first, which I already alluded to, is their outperformance of the benchmark S&P 500. Over the trailing decade, Nvidia’s stock is higher by more than 20,000%, Tesla’s shares have gained north of 1,100%, and both Amazon and Microsoft are within striking distance of 1,000% gains. Meanwhile, the S&P 500 is higher by a comparatively modest 183%.

The second factor that’s powered the Magnificent Seven are their undeniable competitive advantages:

-

Microsoft has become a leader in the cloud, with Azure accounting for a quarter of cloud infrastructure service spending during the September-ended quarter. It’s also one of only two public companies to bear the highest credit rating possible (AAA) from Standard & Poor’s.

-

Apple is consistently the most-dominant domestic smartphone company by market share. On top of its physical product innovation, it offers the largest share repurchase program of any public company in the U.S.

-

Nvidia is the infrastructure foundation of the artificial intelligence (AI) revolution. The company’s A100 and H100 graphics processing units (GPUs) may account for more than a 90% share of GPUs deployed in high-compute data centers this year.

-

Alphabet is something of a jack of all trades. Its internet search engine Google is a veritable monopoly, with a 92% share of worldwide search in February. Alphabet is also the parent of the second most-visited social site (YouTube) and No. 3 global cloud infrastructure service platform (Google Cloud).

-

Amazon, similar to Alphabet, is a key player in multiple categories. Last year, it accounted for close to 38% of U.S. online retail sales. It’s also the leading global cloud infrastructure service provider, with Amazon Web Services comprising a 31% share of worldwide spend in the September-ended quarter.

-

Meta Platforms holds the globe’s top social media real estate. Facebook is the most-visited social site, and its combination of apps, including Instagram, WhatsApp, and Threads, attracts close to 4 billion monthly active users.

-

Tesla is North America’s leading electric-vehicle (EV) maker and the only pure-play EV company that’s achieved recurring profitability on the basis of generally accepted accounting principles (GAAP).

But just because the Magnificent Seven have outperformed when looking in the rearview mirror, it doesn’t mean their outlooks are the same. As we push into the heart of spring, one Magnificent Seven constituent remains historically inexpensive and ripe for the picking, while another highflier may struggle to meet increasingly loftier investor expectations.

The Magnificent Seven stock to buy hand over fist in April: Meta Platforms

Among the seven industry leaders within the Magnificent Seven, the one that can confidently be purchased hand over fist by investors in April (with the purpose of holding shares for years to come) is social media maven Meta Platforms.

Every publicly traded company faces headwinds, and Meta is no exception. The biggest concern for investors is simply the health of the U.S. economy. Last year, Meta generated just shy of 98% of its $134.9 billion in sales from advertising. The ad industry tends to be ultra-sensitive to economic headwinds, with businesses paring back their spending at the first hints of trouble. If a select group of money-based metrics and predictive indicators are correct and a U.S. recession materializes, it could spell trouble for Meta.

But there’s another side to this story that’s even more important. Though economic downturns are normal and will occur whether we want them to or not, they’re historically short-lived. Only three recessions since the end of World War II hit the one-year mark, with none surpassing 18 months. Most periods of growth last for multiple years, which favors ad-based operating models like Meta.

As noted, Meta Platforms has the most-popular social media sites. Facebook recorded 3.07 billion monthly active users (MAUs) in the December-ended quarter, with 3.98 billion MAUs across the entirety of its platforms. Advertisers understand that no social media company offers broader access to consumers than Meta. As a result, it should boast enviable ad-pricing power more often than not.

Investors are also clearly excited about Meta’s AI ambitions. In particular, generative AI solutions give advertisers the ability to tailor their message(s) to individual users. We’re witnessing just the tip of the iceberg in terms of AI utility for Meta.

Something that often gets overlooked about Meta is that it’s swimming in cash. While skeptics have been quick to point to its growing losses at Reality Labs (the company’s augmented/virtual reality and metaverse division), Meta closed out 2023 with more than $65 billion in cash, cash equivalents, and marketable securities, and generated over $71 billion in cash from operations last year. Its cash pile affords it the luxury of taking risks.

The cherry on top is that Meta is still historically cheap, even after more-than-quintupling from its 2022 bear market low. Shares are valued at 13 times estimated cash flow for 2025. This represents an 11% discount to the company’s trailing-five-year cash-flow multiple and is an absolute bargain with earnings slated to grow by an annual average of 26% through 2028.

The Magnificent Seven stock to avoid like the plague in April: Nvidia

However, not all Magnificent Seven members are poised to be winners moving forward. The highflier that’s worth avoiding at all costs in April is megacap outperformer Nvidia.

Don’t get me wrong, there are viable reasons why Nvidia has gained nearly $2 trillion in market cap since the start of 2023. The company’s GPUs are nothing short of a go-to for data centers responsible for training large language models and powering generative AI solutions.

Something else that’s unquestionably helped Nvidia’s sales has been demand for AI-GPUs swamping supply. During the first-half of Nvidia’s fiscal 2024 (ended Jan. 28, 2024), the company’s cost of revenue actually declined! Though GPU production began to pick up during the fiscal fourth quarter, much of the company’s 217% increase in data center sales last year came from scarcity-driven pricing power.

But there are plenty of reasons to believe Nvidia’s headwinds will soon outnumber its tailwinds.

For example, Nvidia’s expanded production in the current fiscal year has the potential to be its undoing. Normally, increased production would lead to higher gross profit. But don’t forget that GPU scarcity is what drove the lion’s share of data center sales growth last year. As new competitors enter the space and Nvidia meets more of its customers’ demands, scarcity will taper and the company’s margins should retrace.

As I pointed out recently, competition is another concern — but not just from external competitors. The biggest threat to Nvidia’s sales may come from its top customers. Microsoft, Meta Platforms, Amazon, and Alphabet collectively account for about 40% of Nvidia’s sales; and they’re all developing AI chips for their in-house data centers. These internally developed chips will either complement Nvidia’s AI infrastructure and reduce the reliance of these four Magnificent Seven stocks on the AI kingpin, or they could replace Nvidia entirely. Either way, we’re likely witnessing a peak in orders from its top customers.

Regulators are capping Nvidia’s upside, too. In September 2022, regulators banned the export of Nvidia’s top-tier A100 and H100 chips to China. Though Nvidia developed toned-down versions of these AI-GPUs, known as the A800 and H800, U.S. regulators also banned the export of these chips in October 2023. Nvidia is missing out on billions of dollars in quarterly sales because of these restrictions.

Last but not least, every next-big-thing investment trend over the last 30 years has worked its way through an early stage bubble. Investors have consistently overestimated the adoption of new innovations/technologies for decades, and artificial intelligence is unlikely to be the exception. Note, I’m not saying AI and Nvidia can’t be wildly successful over the long run. Rather, I’m noting that history suggests Nvidia is in an early stage bubble because AI hasn’t matured as a trend. This makes Nvidia a stock worth avoiding in April.

Should you invest $1,000 in Meta Platforms right now?

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of April 1, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Amazon, and Meta Platforms. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

1 “Magnificent Seven” Stock to Buy Hand Over Fist in April, and 1 to Avoid Like the Plague was originally published by The Motley Fool