CRISPR Therapeutics(NASDAQ: CRSP) is recognized as a pioneer in the field of gene therapy. This biotechnology has the potential to revolutionize medicine through precise modifications of a person’s DNA to treat and cure genetic diseases. In 2023, the company’s Casgevy product for sickle cell disease became the first-ever CRISPR-based therapy approved by the Food and Drug Administration (FDA) as an important company milestone.

Nevertheless, commercialization has been slow, with the market already waiting for the next possible blockbuster drug. At the time of writing, shares of CRISPR Therapeutics are down 46% from their 52-week high, leading investors to wonder what comes next. If you’re considering buying stock in this gene therapy trailblazer, here are three things you should know.

Part of the attraction of CRISPR Therapeutics as an investment is its first-mover advantage, which counts on several patented processes for CRISPR diagnostic and therapeutic applications. The approval of Casgevy, co-developed with Vertex Pharmaceuticals, validated its technology to move forward with a broader pipeline of drug candidates.

A critical component of CRISPR is the requirement that therapies are manufactured using individual patients’ harvested stem cells. CRISPR Therapeutics operates an industrial laboratory facility that provides strategic flexibility to scale operations. Its oncology, cardiology, and diabetes programs have candidates in different stages of clinical study and human trials.

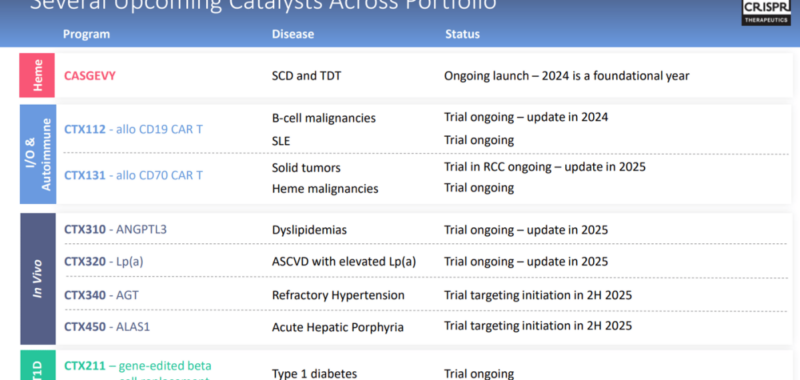

For 2025, the company expects expanded indications for Casgevy, along with updated efficacy data for its candidate portfolio, which could serve as potential catalysts for investors to assess.

Image source: CRISPR Therapeutics.

There’s some optimism that CRISPR Therapeutics is still in the early stages of a significant long-term opportunity. The company’s balance sheet, with $1.9 billion in cash, means CRISPR has the time and capital to take the necessary steps to become commercially sustainable.

On the other hand, the latest financial trends leave a lot to be desired. In the third quarter, CRISPR reported just $602,000 in global revenue, not yet materially capitalizing on the initial launch of Casgevy, marketed and distributed by Vertex.

The update indicates that a single patient has received the commercial therapy, which carries a $2.2 million price tag. This hefty sum can be justified based on its life-saving potential, but it also highlights the economic challenge of widespread adoption. According to Vertex, 40 patients have begun the complex cell collection process that is expected to translate to accelerating collaboration revenue for CRISPR.

Based on Wall Street consensus estimates, from a projected $14 million in revenue this year, CRISPR is projected to bring in $132 million in revenue for 2025 as Casgevy treatments gain traction. Still, that’s not quite enough to make a dent in what are projected to be large financial losses for the next several years. An estimated loss per share of $5.15 for 2024 is only expected to narrow toward a $5.02 loss next year.

That’s not necessarily a problem for a high-growth stock, but it does represent a risk for investors to balance. If sales continue to disappoint, company shares trading at a pricey 31 times next year’s sales as a forward price-to-sales (P/S) ratio could be vulnerable to a deeper sell-off.

CRSP Market Cap data by YCharts

The success of CRISPR Therapeutics will depend on its ability to bring multiple new drugs to the market to support a more viable business model.

At the same time, the company will need to contend with emerging competition from other biotech players pursuing similar CRISPR techniques for drug development. Companies like Intellia Therapeutics and Beam Therapeutics are independently moving forward with their versions of gene-editing technology that could prove more effective for certain diseases.

It’s also uncertain if CRISPR is superior to alternative biotechnologies, like monoclonal antibodies or RNA-based therapies, which have generated recent breakthroughs. Ultimately, CRISPR Therapeutics has a lot of promise but faces a long road to becoming a global biotech leader.

The near-term financial weakness is enough of a reason for me to stay on the sidelines and avoid CRISPR Therapeutics stock for now. The company could very well turn out to be a long-term winner, but the prudent move for investors is to proceed with caution until there is evidence of some sales and earnings momentum. My expectation is for the stock to remain volatile.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $348,112!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,992!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $495,539!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of December 9, 2024

Dan Victor has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Beam Therapeutics, CRISPR Therapeutics, and Intellia Therapeutics. The Motley Fool has a disclosure policy.

3 Things You Need to Know if You Buy CRISPR Therapeutics Today was originally published by The Motley Fool

Heather Ochoa is a news writer at the Failsafe Podcast. She has been writing about politics, health, business, parenting and finance for over a decade. She also loves to go hiking in her free time.