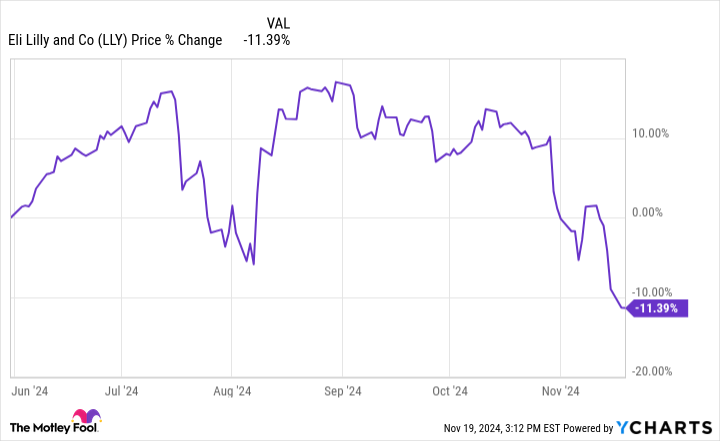

After flying high during the first half of the year, pharmaceutical giant Eli Lilly(NYSE: LLY) has lost some momentum; the company’s shares are down by 11% since June 1. However, the healthcare leader still has plenty of fans on Wall Street, including Israel Englander, the billionaire owner of Millennium Management, a hedge fund.

Millennium Management’s stake in Eli Lilly increased by 86% in the third quarter. Should you follow Englander’s lead and increase your stake (or initiate a position) in Eli Lilly?

Are You Missing The Morning Scoop?Breakfast News delivers it all in a quick, Foolish, and free daily newsletter. Sign Up For Free »

LLY data by YCharts.

Since June 1, Lilly has earned approval for brand-new medicines, including eczema treatment Ebglyss and a potential blockbuster Alzheimer’s disease medicine, Kisunla. It reported several positive data readouts for its new best-selling medicine tirzepatide. And the company’s second-quarter results came with an upward guidance adjustment.

What, then, is the cause of Lilly’s poor performance in the second half of the year? First, its shares look expensive. Eli Lilly’s forward price-to-earnings ratio was recently 54.8. The average for the S&P 500 is 22, and the healthcare industry’s is only 17.4.

LLY PE Ratio (Forward) data by YCharts.

Eli Lilly has been on a tear for a while now, and its shares were bound to face gravity at some point. Some investors likely decided to pocket significant profits before it did.

Second, Lilly’s third-quarter results were below expectations. Revenue grew by 20% year over year to $11.4 billion. That’s not bad by any means, but it wasn’t enough to impress investors, especially considering the company’s valuation. Lilly slightly reducing its guidance for the full year 2024 made things worse, sending the stock off a cliff following its latest quarterly update.

Eli Lilly might or might not rebound by the end of the year. It’s impossible to predict how its shares will perform in the next month, or three, or six. But what if we extend our horizon beyond the next five years? Then we have every reason to think that Lilly can deliver market-beating returns. Let’s consider just three:

First, the company’s tirzepatide — sold under the brand name Mounjaro for diabetes and Zepbound for weight management — is still only getting started. The two brands racked up combined sales of $4.4 billion in the third quarter. Mounjaro was first approved in May 2022, and Zepbound in November 2023.

Excellent data from late-stage trials has already been released for potential new indications for tirzepatide. One of these is reducing the risk of worsening heart failure in adults who have heart failure with preserved ejection fraction and obesity. Tirzepatide also aced phase 3 studies in preventing diabetes in patients with pre-diabetes who are overweight or obese, and it successfully treated sleep apnea in overweight patients.

Tirzepatide is a dual agonist — it mimics the function of two hormones, GLP-1 and GIP — and its success shows the power of this approach. The sky’s the limit if we add other potential indications that haven’t passed late-stage trials yet. Analysts weren’t kidding when they said tirzepatide could hit peak sales of $25 billion.

Second, several of Eli Lilly’s newer medicines not named tirzepatide will eventually make meaningful impacts within the next five years. Kisunla looks promising, but it’s not the only one. Some projections say that ulcerative colitis treatment Omvoh, first approved last year, could generate $1.2 billion in sales by 2029.

Third, Lilly will make significant pipeline progress in the next few years. One of its promising candidates is retatrutide, a triple agonist. Remember that tirzepatide is a dual agonist. Now, Lilly is going one step further with retatrutide, which mimics GLP-1, GIP, and glucagon; the company has dubbed it “triple G.” Progress on this program could be a tailwind for the company. And it’s by no means Eli Lilly’s only exciting candidate.

Thanks to its innovative pipeline, the drugmaker’s lineup should look different in five years. That’s something else that will help drive the stock price higher.

Even with Eli Lilly’s strong prospects, you might hesitate to invest in it because of the high forward P/E, which looks prohibitive. However, its shares don’t seem as expensive once we put things in context. The forward P/E reflects the market’s expectations for the company. If it can match those expectations more often than not, its valuation won’t be too much of a problem. In the third quarter, Eli Lilly’s adjusted earnings per share (EPS) soared to $1.18, compared to just $0.10 in the year-ago period.

Next year, analysts expect EPS to grow by almost 72%. This isn’t surprising, considering tirzepatide’s pace and the fact that several of Lilly’s older medicines are also performing well. The company could keep things up with newer drugs hitting their stride, and tirzepatide earning label expansions. So, in my view, Eli Lilly is worth investing in despite its forward P/E. I’d recommend following billionaire Englander’s lead on this one.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $368,053!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,533!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $484,170!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of November 18, 2024

Prosper Junior Bakiny has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Billionaire Israel Englander Increased His Stake In Eli Lilly During the Third Quarter: Should You? was originally published by The Motley Fool

Heather Ochoa is a news writer at the Failsafe Podcast. She has been writing about politics, health, business, parenting and finance for over a decade. She also loves to go hiking in her free time.