(Bloomberg) — As the Federal Reserve continues to unwind its balance sheet, it’s still dogged by the same issues that it faced more than five years ago.

Most Read from Bloomberg

While market dynamics have evolved, the main issue facing policymakers and investors is how to measure liquidity in the financial system and avoid turmoil that forced the Fed to intervene in September 2019, as the Fed runs down it holdings.

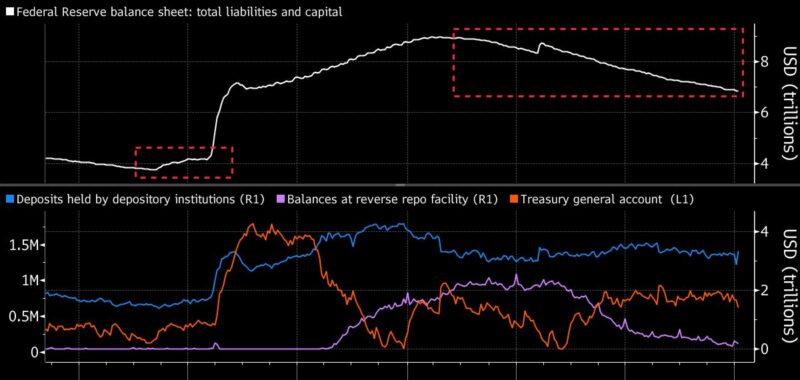

The central bank has reduced its assets by more than $2 trillion since the process known as quantitative tightening began in mid-2022. Now, a plurality of Wall Street strategists expect the Fed to end QT in the first half of the year, given levels at the reverse repo facility, a measure of excess liquidity, being nearly empty and other factors like bank reserves. They also note recent turbulence in the market for repurchase agreements, most notably at the end of September, was not the result of Fed actions as it may have been in 2019.

“Some things may have changed since then, notably the Treasury market is much larger and issuance is very elevated,” said Deutsche Bank strategist Steven Zeng. Constraints on dealers being able to intermediate in the market has also been “a bigger contributor to repo volatility than reserve scarcity, which could be a key difference.

Back in 2019, a confluence of factors, including reserve scarcity as a result of QT — combined with a large corporate tax payment and Treasury auction settlement — led to a liquidity crunch, sending key lending rates skyrocketing and forcing the Fed to intervene to stabilize the market.

Even now it’s still unclear where that point of reserve scarcity lies, though officials have said it’s banks’ lowest comfortable level plus a buffer. Balances are currently $3.33 trillion, a level officials consider to be abundant, and roughly $25 billion below where they were when the unwind started more than two-and-a-half years ago.

To some market participants, the lack of decline has suggested the ideal level of reserves for institutions is much higher than expected and some banks are actually paying higher funding costs in order to hold onto cash. The results of the Fed’s latest Senior Financial Officer survey released last month showed more than one-third of respondents were taking steps to maintain current levels.

The debate over adequate reserves and QT’s stopping point is nothing new. At the January 2019 meeting, then-Fed Governor Lael Brainard cautioned against looking for bank reserves’ steep part of the demand curve, warning that it would “necessarily entail spikes in funds rate volatility” and “new tools would be needed to contain that.”