As investors surely already know, bellwether Intel Corp (INTC) has become the black sheep of the semiconductor family. Late to the game in shifting from CPUs to GPUs, Intel has lost industry leadership to Nvidia (NVDA) and long-term competitor Advanced Micro Devices (AMD). That fact is crystal clear when recognizing that NVDA stock’s market cap is now approximately 40x that of Intel.

With shares of Intel at a low, new leadership at the company, as well as sprinkles of takeover interest since Intel’s dark days of August, many investors may hold optimism for a turnaround in Intel’s valuation. At the current juncture, I prefer to wait but earn income off of a commitment to buy INTC shares at a lower price. Officially, I offer a Hold rating on INTC.

Though the stock has seen bigger market cap losses, Intel stock’s 26% plunge on August 1, 2024, was its biggest downside percentage move in at least the past decade. It was also preceded and followed by trading days with losses greater than 5%. The company has certainly disappointment investors on other occasions, but after reporting their Q2 2024 results, there was little appetite from contrarian investors to buy the dip. Intel’s entire business relevancy was questioned by some analysts as margins fell steeply and the company announced plans for layoffs.

The company also suspended its dividend. Those who took a closer look noticed that Intel’s Free Cash Flow (FCF) had turned negative way back in 2022 and that the company was carrying nearly $30 billion of net debt against declining prospects. Intel had been spending more money than it had been taking in since the beginning of 2023, and the Q2 2024 results essentially served as D-Day for the company’s existing arc and strategy.

Although there’s been substantial pain for investors, INTC shareholders should be thankful that very few large dividend funds/ETFs owned the stock this summer. Otherwise, the selling would have been much worse.

I continue to believe there’s value in Intel. The company has tens of thousands of patents and a longstanding reputation for dependable chips. While the company’s reputation with investors may be severely damaged, its reputation with long-time PC clients should be less harmed. That part of the business should continue to chug along while the company works to regain its bearings and advance its technological competitiveness for the age of AI.

In terms of graphics processing units, I imagine the new leadership team is setting modest goals. Challenging Nvidia and AMD head-on doesn’t seem realistic, at least not in the short term. Working to find an operable niche, such as the Arc B580, which has drawn some favorable reviews within the value space, seems like a good medium-term goal.

I believe the company will have plenty of restructuring options to consider, such as splitting the Foundry and Products businesses, as has been rumored, and/or selling part or all of the company. I think it’s a positive sign that Intel hasn’t rushed to consummate any transaction with Qualcomm (QCOM) or other interested parties yet. No company wants to sell its business at the maximum point of weakness unless absolutely necessary.

One of the things that does concern me is the co-CEO situation that’s now established between Michelle Johnston Holthaus and David Zinsner. With so many important decisions to make, having two people at the helm could result in some stalemates.

Shares of INTC fell slightly below the $20 level in August/September but rallied above $26 after better-than-expected Q3 results in early November. It was relieving for investors to see margins rebound. However, that shine has worn off, and the stock is back in the $ 20 range following the retirement of ex-CEO Pat Gelsinger.

I believe there could be another leg down in INTC shares, potentially as early as this month, due to tax-loss selling. Furthermore, some actively-managed funds may wish to eliminate INTC from their annual reports going into 2025.

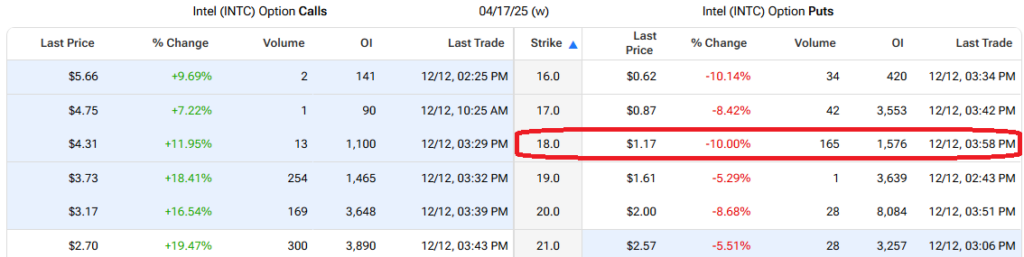

When Intel shares crumbled in August, I sold Put Options at $17.50, and those recently expired, allowing me to bag the Premiums. I’ve recently re-entered that trade, and wrote some April 2025 $18 put options on INTC, which trade at a premium of about $1.17 (or $117 per contract). Should Intel shares drop below $18 and the put options be exercised against me, I’ll have essentially entered a long position on INTC at $16.83. That’s definitely a level I’m comfortable getting in at.

If INTC stock stabilizes and does not drop below $18 by April 17, 2025, I get to keep the ~$117 option premium per contract.

A great number of Wall Street analysts are sitting on the fence when it comes to Intel stock. Of the 29 analysts who cover INTC, there’s only one Buy rating against 22 Hold ratings and six Sell ratings. The average INTC price target is $24.43, however, and represents over 20% upside from the current stock price.

See more INTC analyst ratings

While I believe that Intel can recover, I’m not ready to buy the common stock just yet. There’s a reasonable risk that shares could retest their $18.51 low from early September 2024 as the market weighs the new leadership team. While the company is likely to post a full-year loss for 2024, analysts, on average, are expecting a recovery to an EPS of $0.98 in 2025 (although the estimates are wide-ranging).

That would put INTC stock at a forward P/E of about 21x, which isn’t at all a bargain basement price for a company with the uncertainties this one has. I’d prefer to commit to purchasing INTC at a forward P/E of 17x by selling the April 2025 $18 put options and earning some income if the option isn’t called against me. Officially I carry a Hold rating on Intel shares right now, just like most of Wall Street.

Heather Ochoa is a news writer at the Failsafe Podcast. She has been writing about politics, health, business, parenting and finance for over a decade. She also loves to go hiking in her free time.