With the presidential election season behind us, a major source of uncertainty has been lifted, creating an ideal opportunity for investors to reassess their stock portfolios in light of shifting market conditions.

In this environment, Goldman Sachs analysts are evaluating individual stocks, pinpointing those best positioned to thrive in a growth-oriented market.

We’ve used the TipRanks database to pull up the details on two names that Goldman’s analysts have singled out. Looking at the broader view of them, both are Buy-rated and show nice upside potential. Let’s take a closer look.

KinderCare Learning Companies(KLC)

The first stock we’ll look at, KinderCare, is a for-profit early childhood education company. It was founded in 1969, and from its current base in Portland, Oregon the company oversees a network of educational centers that spans 40 states and can serve up to 200,000 children. This network includes 1,500 early childhood education centers, as well as before- and after-school programs at more than 900 additional sites. In addition, KinderCare operates the Crème Schools, a network of premium early education centers that offer parents and students a variety of themed classrooms and engaging learnings environments. The company’s programs are aimed at children from age 6 weeks up to 12 years.

KinderCare has been in business 55 years, but it only went public earlier this year. The company entered the public trading markets through an IPO in October. The stock, under its new KLC ticker, opened at $27 per share (after being priced for the IPO at $24 per share), with 24 million shares made available. KinderCare raised $576 million in gross proceeds from the offering, which closed on October 10. The company currently has a market cap of $3.12 billion.

Now that KinderCare is a public firm, the company will have to release public earnings reports. The first of these is scheduled for November 20 and will cover 3Q24. Analysts expect the company to report a top line of $669.45 million, along with a modest earnings loss of 2 cents per share.

While we wait to see those results, we can check in with Goldman analyst George Tong, who expects big things from this newly public stock; as he explains KinderCare’s prospects going forward: “We believe KLC is differentiated through its focus on community-based child care centers, which has leaned into the new work-from-home dynamic to drive center occupancy rates to 71%, above pre-COVID levels of 69%. The company’s unique targeting of customers across all income demographics additionally broadens its addressable market and provides access to a stable and growing stream of government child care subsidies. We expect these drivers of occupancy growth to combine with tuition increases, expansion of employer-sponsored and Champions before- and after-school sites, new center openings and acquisitions to drive healthy 6-9% long-term annual revenue growth. Meanwhile, increases in center occupancy rates toward 80% should yield EBITDA margin expansion to the mid-teens from operating leverage, contributing to attractive valuation upside in the shares.”

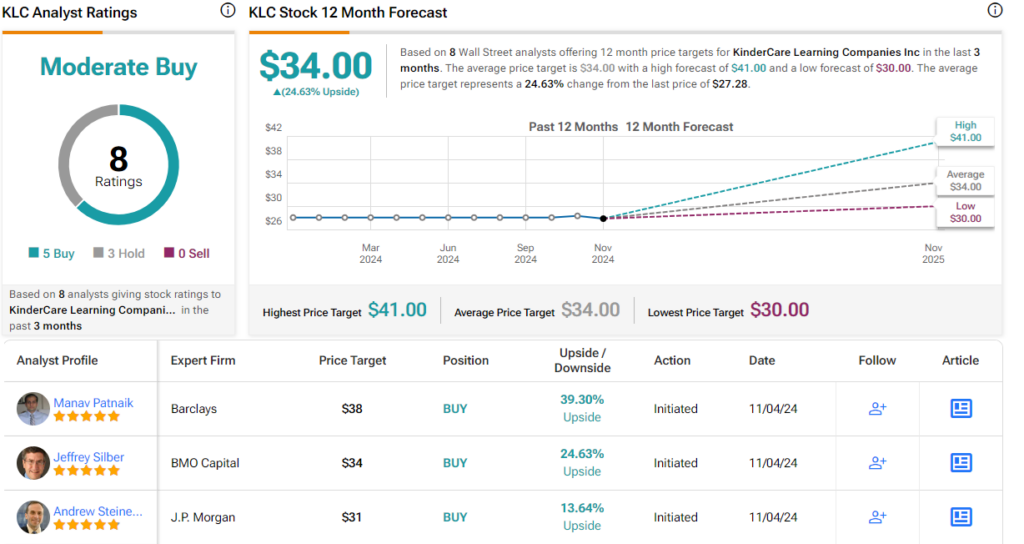

Tong initiates his coverage of KLC with a Buy rating, and his price target of $41 points toward a one-year gain of 49%. (To watch Tong’s track record, click here)

In its short time on the markets, KLC has picked up 8 analyst reviews – and these include 5 Buys and 3 Holds for a Moderate Buy consensus rating. The stock is trading for $27.28 and its $34 average target price implies an upside of 24.5% on the one-year horizon. (See KLC stock forecast.)

LivaNova(LIVN)

Say ‘biotech,’ and most of us will immediately focus on the pharmaceutical industry. But biotechnology includes more than just new drug research – a big part of it is the development and introduction of new medical devices. LivaNova plays an important role in the medical device niche, particularly in the area of neuromodulation.

The company is best known to the public for its VNS (vagus nerve stimulation) products, used in the treatment of epilepsy. This frequently dangerous central nervous system condition is usually treated through medication – but for some patients, epilepsy is drug-resistant. VNS devices operate through direct stimulation of the nervous system, providing an electrical stimulation when a seizure is imminent. The system includes an implanted device that both monitors brain activity and provides the needed stimulation through the vagus nerve. The device is implanted in the upper chest, like a pacemaker, and has demonstrated effectiveness for over 20 years. LivaNova is a leader in VNS technology and device development.

In addition to using VNS to treat drug-resistant epilepsy, LivaNova is also pioneering the use of the technology to treat depression. Chronic depression is notoriously difficult to treat, and many patients will cycle through multiple medication regimes – only to find that none help. LivaNova’s VNS implant can be used to send a mild electrical stimulation to the brain through the vagus nerve – which connects to areas of the brain that control mood. The stimulation device has shown potential in this indication.

VNS device treatments, a vital part of LivaNova’s business, have been used in well over 100,000 patients, including over 30,000 children. The safety and efficacy of the treatment has been demonstrated repeatedly over the past 25 years. That said, this treatment is typically used in patients whose conditions have proven resistant to more traditional therapies.

In addition to its VNS segment, LivaNova also produces and markets the Essenz Perfusion System, a heart-lung machine designed to maintain operative patients’ circulatory and lung functions during surgery. The machine system is designed for both ease of use and redundant backups, with controls for various functions kept separate to avoid confusion. The Essenz machine is state-of-the art, and builds on LivaNova’s long history of reliability.

In its last reported quarter, 3Q24, LivaNova generated revenues of $318.1 million, up more than 11% year-over-year. Of this total, $172.2 million was generated on the cardiopulmonary side, while $139.9 million came from the neuromodulation side. $6 million in revenue was listed as ‘other.’ The company’s bottom line, the non-GAAP EPS of 90 cents per share, was up from 73 cents per share in the year-ago period.

Covering this stock for GS, analyst David Roman notes that the company has seen headwinds in its overall stock performance this year. He says of LivaNova, “LIVN shares have struggled to find periods of outperformance, as strategic shifts in the business and pipeline setbacks have put downward pressure on earnings and the stock’s P/E multiple. As the business produces consistent results and the margin profile is enhanced, we think this period of underperformance fades into the rear view mirror.”

Roman is upbeat for the long term, and adds, “Looking ahead, we see LivaNova’s base business generating approximately 5% top-line growth from stable-end markets and de novo neuromodulation implants as well as a near-term bolus of growth from an identifiable product cycle upgrade in cardiopulmonary (52% of sales). Further revenue growth could stem from discrete pipeline initiatives and share capture that could drive upside to our above consensus forecasts. Sustained top-line growth, improved mix, and more targeted P&L management should drive a period of outsized EPS growth (~14% per GSe through 2027).”

Quantifying his stance, the Goldman analyst puts a Buy rating on LIVN stock, and he complements that with a price target of $65, suggesting a one-year upside of 25.5%. (To watch Roman’s track record, click here)

The broad view on the Street is even more upbeat, setting a Strong Buy consensus rating here based on 7 reviews that include 6 to Buy against just one to Hold. The stock’s $51.81 trading price and $70 average price target combine to give an upside potential of 35% for the coming year. (See LIVN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Heather Ochoa is a news writer at the Failsafe Podcast. She has been writing about politics, health, business, parenting and finance for over a decade. She also loves to go hiking in her free time.