Dell Technologies(NYSE: DELL) has been in sizzling form on the stock market so far in 2024, rising an impressive 76% as of this writing. This occurred thanks to a turnaround in the company’s fortunes due to the growing demand for its server solutions used for mounting artificial intelligence (AI) chips.

The stock’s 2024 rally will be put to the test when Dell releases its fiscal 2025 third-quarter results on Tuesday, Nov. 26. Let’s see what investors can expect from Dell when it releases its quarterly report, and check if its guidance is going to be solid enough to help it sustain its impressive rally.

Are You Missing The Morning Scoop? Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

When Dell released its fiscal 2025 second-quarter results in August, management pointed out that the company’s growth is likely to pick up in the second half of the fiscal year. It guided for fiscal Q3 revenue of $24.5 billion at the midpoint of its guidance range, which would be a 10% jump from the same quarter last year.

Dell expects adjusted earnings to land at $2 per share at the midpoint. Consensus estimates compiled by Yahoo! Finance, however, are expecting Dell to deliver $2.04 per share in earnings on revenue of $24.7 billion. It won’t be surprising to see the company beat Wall Street’s increased expectations, thanks to the solid demand for its AI servers.

For instance, in fiscal Q2, Dell sold $3.2 billion worth of AI servers, as compared to $2.6 billion in Q1. A strong performance seems to be in the cards, once again, as the company finished Q2 with an AI server order backlog of $3.8 billion.

It also pointed out that it has a potential revenue pipeline that “has grown to several multiples of our backlog.” If Dell manages to ship more AI servers on the back of an improved supply chain, there’s a good chance it can post better-than-expected numbers.

Another factor that could play in Dell’s favor involves the problems that its rival Super Micro Computer(NASDAQ: SMCI) is facing. Supermicro stock has plummeted on negative news, including accusations of accounting manipulation, the resignation of its auditor, and management’s failure to file the annual report within the stipulated timeline.

It now appears that Supermicro’s customers are shifting their orders away from the company. As reported by Tom’s Hardware, Elon Musk’s xAI has reportedly taken $6 billion worth of AI server orders elsewhere from Supermicro. The report adds that Dell could be one of the biggest beneficiaries of such a development as it’s one of the largest server manufacturers in the world.

Moreover, Dell reportedly commands half of the AI server orders from Elon Musk-led companies (with Supermicro controlling the other half). If Supermicro is indeed losing orders for AI servers, the chances of Dell delivering better-than-expected results and guidance are stronger.

With the stage set for Dell to deliver better-than-expected results, investors should also note that a negative reaction to the company’s results should be treated as a buying opportunity. That’s because the global AI server market is forecast to hit $177 billion in annual revenue by 2032, according to Global Market Insights, up from $38 billion last year.

This explains why Dell management remarked on the last earnings conference call that it has a solid pipeline of customers for its AI servers that’s significantly larger than its backlog. If Dell can convert that pipeline into actual revenue and win a bigger share of the AI server market, it could see a long-term acceleration in its revenue and earnings growth.

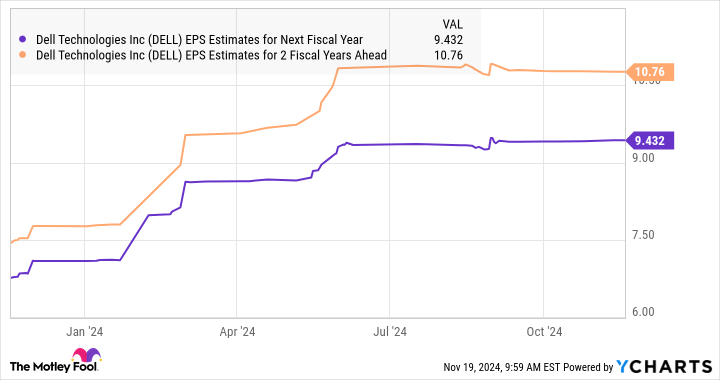

It’s worth noting that Dell’s earnings in fiscal 2024 fell 6% from the previous year to $7.13 per share. The company expects to deliver $7.80 per share in earnings in fiscal 2025, which would be an improvement of 9% from the previous year at the midpoint. The forecast for the next couple of years points toward a stronger jump in Dell’s bottom line.

DELL Eearnings-Per-Share Estimates for Next Fiscal Year data by YCharts.

With Dell currently trading at 25 times trailing earnings and 13 times forward earnings, investors are getting a good deal on this AI stock right now. They may want to grab it with both hands, as it looks likely to take off after releasing its results on Nov. 26.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $378,269!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,369!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $476,653!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of November 18, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Prediction: This Artificial Intelligence (AI) Stock Is Going to Soar Higher After Nov. 26 was originally published by The Motley Fool

Heather Ochoa is a news writer at the Failsafe Podcast. She has been writing about politics, health, business, parenting and finance for over a decade. She also loves to go hiking in her free time.