Furious investments in data centers are spurred by our growing need for data storage and processing power and the tremendous requirements of artificial intelligence (AI) programs. While some data centers are relatively small, others are larger than 100,000 square feet (often millions of square feet). Tech titans like Microsoft, Amazon,Alphabet, and Meta typically construct these hyperscale data centers.

For instance, in 2025, Meta will break ground on an $800 million, 715,000-square-foot campus in South Carolina, and Microsoft will begin a $1 billion project in La Porte, Indiana.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

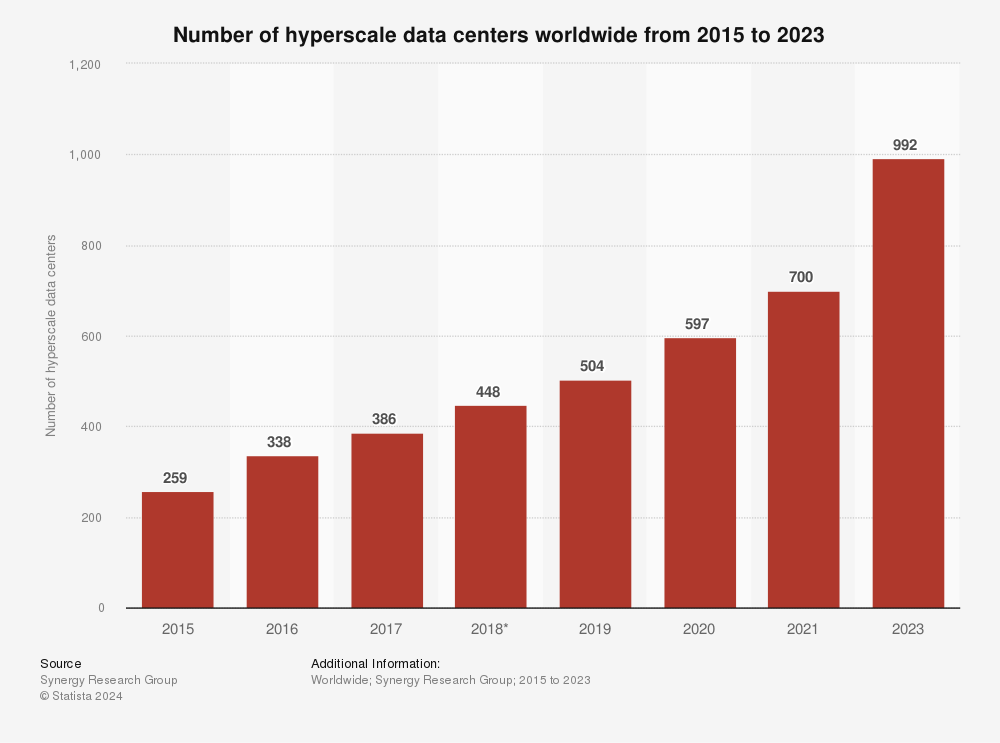

As shown below, Hyperscale centers have spiked recently.

Statista.

This number eclipsed 1,000 in 2024 and is forecast to grow by 120 to 130 annually. These centers require infrastructure like servers, storage, and racking, so investors should be excited about the opportunity.

Dell Technologies(NYSE: DELL) is a major supplier to the industry, along with Super Micro Computer. Supermicro has some well-documented challenges now, and Dell could be a key beneficiary. Here are some things to know.

Supermicro’s setbacks are well documented, so I won’t dwell too much on them. Here is a brief timeline:

August: Hindenburg Research released a scathing short report, and Supermicro delayed its annual 10-K filing.

September: Nasdaq notified the company that it could be delisted for its delayed filing.

October: Supermicro’s audit firm, Ernst & Young, resigned.

November: The company delayed its quarterly 10-Q filing.

As of this writing, the stock trades 84% off its 2024 high.

SMCI data by YCharts

None of these are smoking guns alone; however, these are serious concerns.

It makes sense for a data center operator to avoid the noise and choose Dell for its infrastructure needs over Supermicro, which reported $5.3 billion in sales in the fiscal 2024 fourth quarter ($15 billion for the fiscal year), with 64% attributed to large data centers. Dell’s Infrastructure Solutions Group earned $11.6 billion in its most recent quarter, so potentially picking up billions of dollars in revenue from a competitor would be an enormous boon.

Dell’s recent results are solid, but it’s what analysts estimate for the next several years that is most exciting. Revenue grew 9% in the second quarter of fiscal 2025 to $25 billion, while diluted earnings per share (EPS) rose 86% to $1.17. As expected, the Infrastructure Solutions Group, which serves data centers, hit record sales of $11.6 billion on impressive 38% year-over-year growth.

Analysts expect $7.87 in EPS this fiscal year and then even more:

DELL annual EPS estimates; data by YCharts.

This is why 20 of 25 analysts rate the stock a buy or strong buy with an average target of $145 per share, or 10% above the stock’s price at the time of this writing. However, analyst estimates may not yet account for the potential of Dell to take market share from Supermicro. This gives the stock more room to run.

Dell is also attractive because it pays dividends and repurchases stock. The company intends to return 80% of adjusted free cash flow to shareholders and grow the dividend, which currently yields 1.3%, by 10% annually. Adjusted free cash flow hit $5.6 billion in fiscal 2024 and $3.7 billion through two quarters of fiscal 2025. Free cash flow should grow significantly along with earnings.

Data center infrastructure needs are exploding, and Dell looks like the company in the best position to benefit over the next several years. Tech investors should consider a long-term position in the stock.

Before you buy stock in Dell Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dell Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $869,885!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of November 18, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Bradley Guichard has positions in Amazon and Dell Technologies. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Prediction: This Company Will Be the Biggest Beneficiary of Super Micro Computer’s Problems was originally published by The Motley Fool

Heather Ochoa is a news writer at the Failsafe Podcast. She has been writing about politics, health, business, parenting and finance for over a decade. She also loves to go hiking in her free time.