Buy-side stock analysts can be helpful. They often come with advanced financial skills and training, vetted through many years or even decades of experience in money management. So, it can make sense to check out what Wall Street professionals are saying about your next investing idea.

That said, they don’t always have the right answers or the best analysis. In most cases, analysts’ consensus stock ratings are backward-looking reviews of recent events — not insightful projections of what could happen in the future.

The Street was only mildly enthusiastic about Nvidia before the ChatGPT release made it a market darling. When Netflix (NASDAQ: NFLX) was a no-brainer buy in the wake of the Qwikster crisis of 2011, the consensus analyst view on that stock was a hold, with a slight leaning to the bearish side. That turned out to be a fantastic time to buy Netflix stock, with returns of more than 5,300% in the next 12 years.

So, the analysts don’t always get it right, not even when their average recommendation is unusually bearish. On that note, Wall Street’s attitude toward computer-managed insurance company Lemonade (NYSE: LMND) reminds me of the old Netflix miscalculations right now. The consensus recommendation is a hold, with slightly more sell than buy outliers.

I think this recommendation will go down as one of the classic blunders. Here’s why Lemonade’s stock looks ready to soar from this low spot.

The market’s consensus on Lemonade

Lemonade’s current analyst rating is a slightly bearish hold. Among 10 analyst firms offering a rating on the stock, six are sticking with the middle-of-the-road hold advice. One stands out with a buy rating, while three suggest some sort of sell action.

Judging by their questions on Lemonade’s latest earnings call, the bearish analysts worry about the company’s exposure to catastrophic damage claims, or CAT. A plethora of damaging winter storms led to an unfavorable gross loss ratio, weighing on Lemonade’s bottom-line profitability.

It’s harder to determine the motivation for the lone bullish rating from Karol Chmiel of Citizens JMP group. The analyst rarely asks questions on the company’s earnings calls, and JMP isn’t keen on publishing its research reports publicly.

The bullish case for Lemonade

So, here’s my own Lemonade analysis instead. I’m a longtime shareholder of this innovative insurance company, which started relying on artificial intelligence (AI) to manage its core business long before it was cool.

Lemonade’s automated approach instantly makes sense to me from the consumer’s point of view. Traditional insurance experts, like Progressive or Allstate, depend on human agents to recruit, sign up, assess, and manage customers. The process is prone to human error at every stage, and taking the emotion out of this business with computerized automation makes a ton of sense.

The deep learning systems handling Lemonade’s insurance policies and claims are not perfect, either. In fact, these systems have made a lot of imperfect decisions so far, resulting in painfully high loss ratios and negative bottom-line results.

But here’s the thing — Lemonade’s insurance systems are making suboptimal decisions for the company in the early going while building a larger knowledge base and a deeper understanding of the insurance business. Every insurance business grows more financially stable as its operations scale up, and that’s only more true for Lemonade, with its direct reliance on real-world data from actual customers and concrete insurance claims.

So, it’s a learning process, and Lemonade is far from building the perfect robotic insurance solution today. At the same time, the company is indeed scaling up quickly and setting itself up for long-term success.

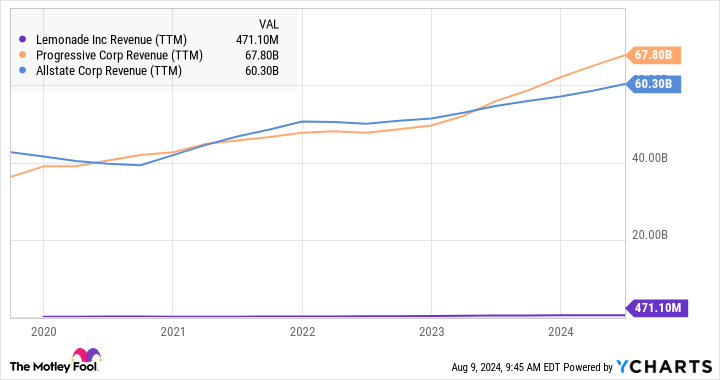

How Lemonade measures up against industry giants

I mean, check out Lemonade’s revenues compared to the insurance giants I mentioned earlier. This business is basically a rounding error next to Progressive’s and Allstate’s massive revenue streams:

But the picture changes dramatically if I switch to percentage-based revenue growth instead. This time, it’s the giants of this industry that look flat-footed:

Lemonade is indeed growing its business in many ways. In the recent second-quarter report, its customer count rose by 14% year over year. The average insurance premium per customer increased by 8%, resulting in a 22% boost to the total amount of in-force premiums.

And the policy-managing machines are learning a lot from this growing customer base. Lemonade’s gross profit doubled in the second quarter, the net loss ratio is improving over time, and the company achieved $4 million of positive net cash flow in this report.

Why I think Lemonade is a fantastic buy today

My view of Lemonade is quite simple: I see an innovative AI expert striving to shake up the enormous and often inefficient insurance industry. The company is young and has a lot to learn, but the recent production of cash-based profits tells me Lemonade is getting a grip on the situation.

So, I’m convinced that Lemonade is a future insurance giant in the making, and bearish analysts are making another Netflix-like mistake. Lemonade’s stock is a no-brainer buy right now, and I can’t wait to see the company sweeten its AI-driven insurance recipes over the next few years. One of these days, AI-managed insurance could very well become the industry standard, and Lemonade would stand out as a grizzled leader at that point.

Should you invest $1,000 in Lemonade right now?

Before you buy stock in Lemonade, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lemonade wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $641,864!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of August 6, 2024

Anders Bylund has positions in Lemonade, Netflix, and Nvidia. The Motley Fool has positions in and recommends Lemonade, Netflix, and Nvidia. The Motley Fool recommends Progressive. The Motley Fool has a disclosure policy.

Wall Street Analysts Are Bearish on This Artificial Intelligence (AI) Stock. Here’s Why I’m Not. was originally published by The Motley Fool