(Bloomberg) — Jerome Powell delivered exactly what traders up and down Wall Street had long hoped for: A big interest-rate cut that would justify this year’s steep rally in stocks and bonds as the era of tight monetary policy finally began to reverse.

Most Read from Bloomberg

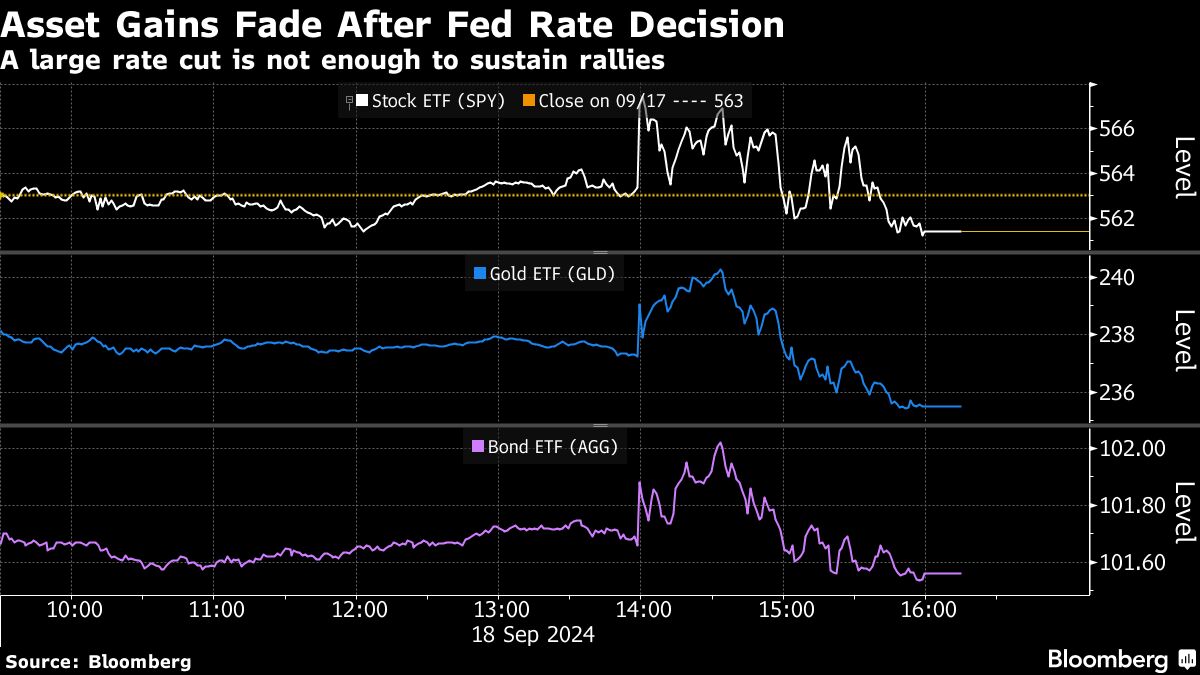

Equities, especially those of economically sensitive companies, briefly surged, driving the S&P 500 up as much as 1%. Ditto bonds, while the prospect of easy money ahead initially pushed up speculative assets like crypto.

Yet by the time the trading day ended, the gains fizzled as a more sobering economic and market reality sunk in. Even with the half-point rate cut — the kind of aggressive move usually reserved for a recession or crisis — and more on the way, the investment backdrop was no more clear cut than it was before.

Stock prices are already near record highs. The economy is losing a little steam. And it’s no sure thing that the rock-bottom rates swept away by post-pandemic inflation will come back anytime soon.

From stocks to Treasuries, corporate bonds to commodities, every major asset was down Wednesday. While the scale of the declines were minor, a concerted pullback like that hadn’t followed a Fed policy decision since June 2021. On Thursday, equities gained some momentum, but the dollar fell and Treasuries were slightly up.

Of particular concern to traders were comments from Powell that coincided with the reversal in the stock and bond markets: that nobody should expect the Fed to make a habit of half-point reductions in the future, and that the neutral level of interest rates is likely higher than it was before the pandemic.

“The important point here is that there’s the action, in the 50 basis points, and the expectation in what was priced in,” said Jeffrey Rosenberg, a portfolio manager at BlackRock Inc., on Bloomberg Television. “This is a little bit disappointing relative to what’s been built up in bond expectations.”

That was clear in the immediate reaction to the Fed’s announcement. Two-year Treasury notes, among the most sensitive to policy changes, rallied in the aftermath, but have failed to hold the gains.

Powell was upbeat about the economy and waved off recession fears, tempering the market’s expectations for where it’s heading. During his press conference, he said the central bank is confident “strength in the labor market can be maintained in a context of moderate growth and inflation moving sustainably down to 2%.” At the same time, he cautioned against assuming the half-point move set a pace that policymakers would continue — underscoring that everything would hinge on how the data come in.

The bond market had already been baking in a series of rate cuts and bets on Wednesday’s move had piled up so heavily that it was effectively already accounted for. The two-year Treasury yield, for example, had already tumbled from more than 5% in late April, enough to reflect several rate cuts.

“It was always going to be difficult for Powell to ‘out dove’ the bond market given how much it had moved in the last six weeks or so,” said Michael de Pass, global head of rates trading at Citadel Securities.

While the economy doesn’t seem in obvious need of stimulus, there are signs of a weakening trend. The three-month average gain in non-farm payrolls stands at the lowest since 2020 and gauges of factory output have slipped.

At the same time, the unemployment rate is just 4.2%, gross domestic product in 2024 is forecast to expand at the same rate as last year, and analysts currently peg 2025 earnings growth in the S&P 500 at an especially robust 14%. That sanguine backdrop had led investors to bid up stocks to nearly unprecedented valuations at the time of a first rate cut: more than 25 times earnings over the last four quarters.

That may reflect another anomaly of the current moment: the Fed has pushed rates so high — around 5.3% before Wednesday’s move — that it has made traders confident it has plenty of room to cut if the economy sputters.

“While we all can debate the warranted speed of rate cuts out of the gate, the reality is the direction of travel for policy rates is lower,” said Charlie Ripley, senior investment strategist for Allianz Investment Management. “The track record from this Fed has shown they haven’t historically been the fastest out of the gate, but they have exhibited the ability to dial up the pace when deemed necessary.”

Traders however have struggled to predict the Fed’s path since inflation surged in the wake of the pandemic, and Powell’s dependence on incoming data means that it will be no easier even now that it’s changed course.

Policymakers penciled in an additional percentage point of cuts in 2025, according to their median forecast. Bond traders, however, are still counting on a more aggressive pace.

“A more prolonged and predictable easing cycle is at hand,” said Jack McIntyre, portfolio manager at Brandywine Global Investment Management. “It now will be a battle between market expectations and the Fed, with employment data — not inflation data —determining which side is right.”

–With assistance from Vildana Hajric, Liz Capo McCormick, Emily Graffeo, Aline Oyamada and Cecile Gutscher.

(Updates with Thursday’s market moves in fifth paragraph.)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.